No one likes paying taxes, but for taxpayers who live on a fixed income having to pay a a large tax bill can mean real financial hardship – and the majority of Canadians who live on fixed incomes are, of course, those who are over 65 and retired.

No one likes paying taxes, but for taxpayers who live on a fixed income having to pay a a large tax bill can mean real financial hardship – and the majority of Canadians who live on fixed incomes are, of course, those who are over 65 and retired.

For the past two years, Canadians have had to continually adjust their household budgets to accommodate price increases for nearly all goods and services.

Most Canadians don’t turn their attention to their taxes until sometime around the end of March or the beginning of April, in time to complete the return for 2023 ahead of the April 30, 2024 filing deadline.

While owning one’s own home brings with it many intangible benefits, home ownership also provides some very significant financial advantages. Specifically, it provides the opportunity to accumulate wealth through increases in home equity, and to realize that wealth on a truly tax-free basis.

While our tax laws require Canadian residents to complete and file a T1 tax return form each spring, that return form is never exactly the same from year to year. Some of the changes found in each year’s T1 are the result of the indexing of many aspects of our tax system, as income brackets and tax credit amounts are increased to reflect the rate of inflation during the previous year.

Each year, the Canada Revenue Agency publishes a statistical summary of the tax filing patterns of Canadians during the previous filing season. The final statistics for 2023 show that the vast majority of Canadian individual income tax returns – just over 92%, or just under 30 million returns – were filed by electronic means, using one or the other of the CRA’s web-based filing methods. About 2.5 million returns – or just under 8% – were paper-filed.

Income tax is a big-ticket item for most retired Canadians. Especially for those who are no longer paying a mortgage, the annual tax bill may be the single biggest expenditure they are required to make each year.

If there is one invariable “rule” of financial and retirement planning of which most Canadians are aware, it is the unquestioned wisdom of making regular contributions to one’s registered retirement savings plan (RRSP). And it is true that for several decades the RRSP was the only tax-sheltered savings and investment vehicle available to most individual Canadians.

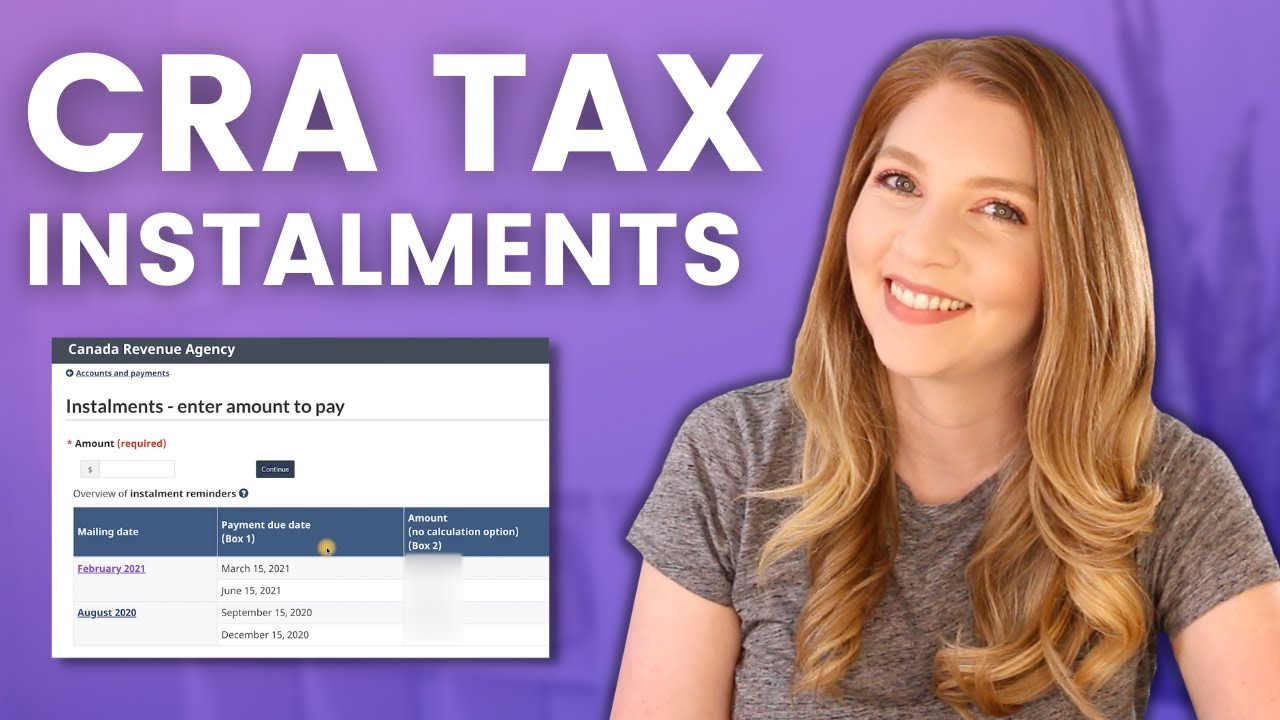

Sometime during the month of February, millions of Canadians will receive some unexpected mail from the Canada Revenue Agency (CRA). That mail, entitled simply “Instalment Reminder”, will set out the amount of instalment payments of income tax to be paid by the recipient taxpayer by March 15 and June 15 of this year.

The Employment Insurance (EI) premium rate for 2024 is set at 1.66%.

Yearly maximum insurable earnings are set at $63,200, making the maximum employee premium $1,049.12.

As in previous years, employer premiums are 1.4 times the employee premium. The maximum employer premium for 2024 is therefore $1,468.77.

The information presented is only of a general nature, may omit many details and special rules, is current only as of its published date, and accordingly cannot be regarded as legal or tax advice. Please contact our office for more information on this subject and how it pertains to your specific tax or financial situation.